Read time: 6 mins

Read time: 6 mins

The Evolution Of The Fintech Industry

While the Oxford Fintech Programme from Saïd Business School, University of Oxford focuses on enabling you to add to the future of the fintech revolution, it’s important to have an awareness of where financial technology has come from, and the journey it’s taken to get to where it is now, and to get an idea of possible fintech trends of the future.

The fintech revolution begins in the 1800s

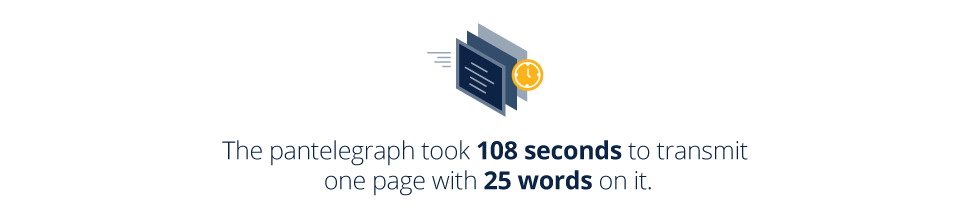

The history of fintech innovation goes as far back the 1860s, when a device known as the pantelegraph was invented by Giovanni Caselli.

Used predominantly to verify signatures in banking transactions by sending and receiving transmissions on telegraph cables, this invention is widely regarded to be the first step in the journey towards fintech as we know it today.1 It was a small step – the device was notoriously slow, meaning a sheet of paper with about 25 handwritten words took about 108 seconds to transmit.

The next turn in the fintech revolution took place in the late 1800s, when consumers and merchants began exchanging goods and services for credit using items known as charge plates and charge coins.

Used until the early 1960s, charge plates were aluminium or white metal plates embossed with a customer’s name and address on the front, and a paperboard insert on the back with the issuer’s name and cardholder’s signature. Charge coins were of similar function, bearing the customer’s identification number and an image associated with the vendor, and were roughly the same size and shape as modern coins.2

These coins and plates were mostly issued and used by department stores, but also held weight with some oil companies.

Fintech innovations of the 1900s

The next early fintech innovation was developed in 1918, when the United States Federal Reserve Banks devised a system to move funds electronically, known then as the Federal Reserve Wire Network, or Fedwire more recently.3

Connecting all 12 Reserve Banks across the country, the Morse code-based system was used as a real-time gross settlement funds transfer system until the 1970s, thereafter it shifted from telegraphy towards telex, and finally to computer operations and proprietary communications networks.

The system operated without major hitches until the early 1980s, when it began experiencing bottlenecking due to the amount of requests being received. In response, the US Federal Reserve made some changes and upgrades to the system – and continued to do so into the future as new technology like internet protocol and distributed processing arose. This ensured the Fedwire system a place in the modern fintech landscape of today.

Not long after the advent of Fedwire, in arguably the first allusion to ‘financial technology’ as a standalone concept, economist John Maynard Keynes wrote about the link between finance and technology in 1919, in his book The Economic Consequences of the Peace.4

The emergence of modern fintech trends in the late 1900s

In 1950, the first iteration of the credit card was introduced by Diner’s Club Inc.5 This signalled the beginning of the emergence of modern fintech trends as we know them today.

Even though – as previously mentioned – credit was not a new concept, it was quite a laborious and segmented process. The introduction of the first universal credit card meant credit could be traded on at a variety of establishments. This was later followed in 1958 by a travel and entertainment card of the same nature, offered by American Express Company.

The 1960s saw the introduction of the Quotron, the global telex network, and the first ATM.

The Quotron was the first product to offer stockbrokers and money managers stock market quotes to an electronic screen in 1960, instead of a printed ticker tape.6 The speed and agility accompanying digital recall meant brokers could receive up-to-the-minute prices for securities. By 1986, Quotron was renting 100,000 terminals to the brokerage industry, equating to roughly 60% of the 1986 market, which attracted the attention of Citicorp, who acquired them soon after.7

Unfortunately, the company was slow to move from their dedicated terminal system to the PC, and Citicorp later paid Reuters Holdings more than $100 million to pass off the ailing Quotron, who now employ the Quotron as their trading floor terminal.

The telex network replaced the telegraph as the standard of long-distance instantaneous communication of information in 1966 – the difference being that any user on any telex exchange could deliver messages to any other user all around the world. This flexibility opened the doors for global communication of financial transactions and information. The telex is still in use today, but not in the same sense as its original product. It has mostly been superseded by fax and email.

1967 saw the first automated teller machine (ATM) installed, by Barclays Bank in its Enfield Town branch in North London.8 To receive their cash from the machine, users were required to insert paper cheques issued by a teller or cashier. These cheques were marked with carbon-14 as a security measure and to improve machine readability. This security measure was later paired with a 6-digit pin for extra protection.

The lead engineer credited with this particular fintech invention, John Shepherd-Barron, said at the time: “It struck me there must be a way I could get my own money, anywhere in the world or the UK. I hit upon the idea of a chocolate bar dispenser, but replacing chocolate with cash.”9

It struck me there must be a way I could get my own money, anywhere in the world or the UK, I hit upon the idea of a chocolate bar dispenser, but replacing chocolate with cash

JOHN SHEPHERD – BARRON

INVENTOR OF THE ATM

A new era of fintech trends in the 1970s

One of the biggest transformations of the fintech landscape took place in 1971, with the establishment of the National Association of Securities Dealers Automated Quotations – or NASDAQ as most of the world knows it.10

As the world’s first electronic stock market, it helped reduce the spread (the difference between bidding price and asking price of a stock) and as such heralded the end of fixed securities commissions. The NASDAQ helped modernise the IPO (Initial Public Offering) and attracted new growth companies like Microsoft, Dell, Cisco, Oracle and Apple.

Fintech introduces the world to online banking and trading in the 80s

The early 1980s saw two large steps taken in the fintech revolution: E-Trade and online banking.

E-Trade, originally founded under the name of TradePlus, became the first online stock brokerage firm in 1982.11 The public company servicing self-directed investors still serves customers today, and fielded 164,134 average trades in 2016, bringing in almost US$2 billion.12

In 1983, customers of the Nottingham Building Society were the first to get access to online banking, provided by the Bank of Scotland and known as Homelink.13 Online banking was initially introduced in the US in 1983 by Chemical Bank, but due to a lack of customer draw, canned the idea in 1989 – and other banks had a similar experience. In the wake of the success of internet banking in the UK, the majority of banks in the US set up their first transactional websites for internet banking in the late 1990s.14

Fintech innovations in the new millenium

Thereafter, the 2000s are littered with fintech innovation after fintech innovation, most of which are well known today. However, some breakthroughs are more noteworthy than others, including:

– 2009 saw version 0.1 of the now-dominant cryptocurrency Bitcoin released15

– 2011 heralded the development of Google Pay Send (formerly known as Google Wallet), a fintech innovation that allowed smartphones users with NFC (Near-Field Communication) chips in their devices to make tap payments16

– 2017 brought with it the ‘smile to pay’ service from Alibaba, a fintech innovation that enables users to pay simply by smiling at a 3D camera17

If the current fintech trend in new ICOs (Initial Coin Offerings) is anything to go by, the future of the fintech revolution is blindingly bright, and should be exciting to any burgeoning fintech enthusiast or business person. Take a look at this animated graph for a striking visual representation of what the future of fintech, specifically cryptocurrencies and ICOs, could hold for the global economy.

The adoption of fintech trends such as telex network, ATMs and automated trading is testament to not only the willingness of the financial industry to adapt and evolve, but to the speed at which it does so. As a professional in any industry, a solid understanding of fintech innovation possibilities and case studies and their impacts on markets and the future of money will stand you in good stead for a future of inevitable financial disruption.

Step beyond current financial technology disruption and prepare for future financial services priorities with the Harvard VPAL FinTech course.