Read time: 7 mins

Read time: 7 mins

Blockchain Explained: What You Need to Know

The global economy is built on a foundation of exchange – the exchange of funds, information, and resources. But many forms of trade have problems with fraud or theft.

Because of this, society has developed ways to learn more about trading partners so that you can make informed decisions about whether or not you can trade safely with them.You can do this in many ways – by checking the seller rating of a vendor on Amazon before purchasing their product; signing multiple copies of a contract so there is undeniable proof of an agreement; building institutions to create safeguards around the exchange of value.

According to blockchain entrepreneur and researcher Bettina Warburg, the advent of blockchain technology allows us, for the first time, to “lower uncertainty not just with political and economic institutions, like our banks, our corporations, our governments, but we can do it with technology alone.”1

What is blockchain?

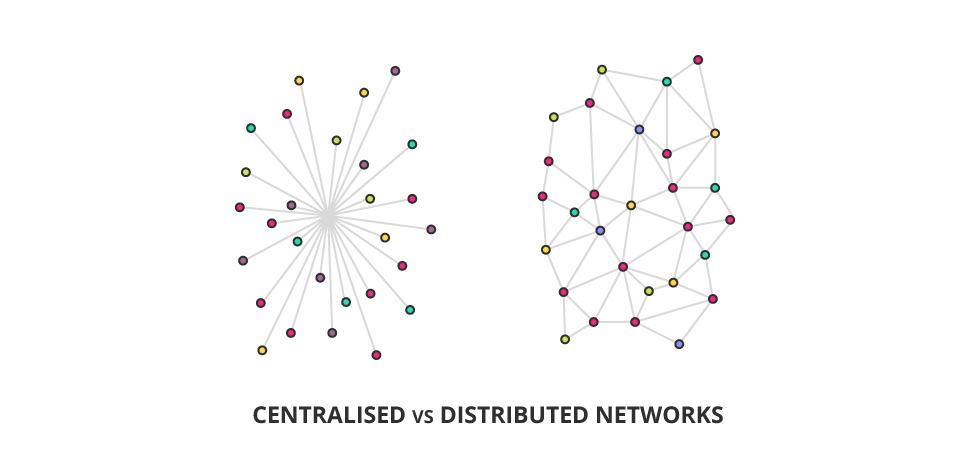

Blockchain can be defined simply as a digital ledger system. It can be used to track not just financial transactions, but any transaction of information, making it possible to share documents and personal information as well as cryptocurrencies.2 What makes this system so different, is its fully distributed ownership rights. The information in the blockchain ledger is not shared to a network from one single access point, but hosted across a distributed network of devices, making the system almost tamper-proof.3

Technology Futurist Ian Khan explains, “The most critical area where blockchain helps is to guarantee the validity of a transaction by recording it not only on a main register but a connected distributed system of registers, all of which are connected through a secure validation mechanism.”4

How does blockchain work?

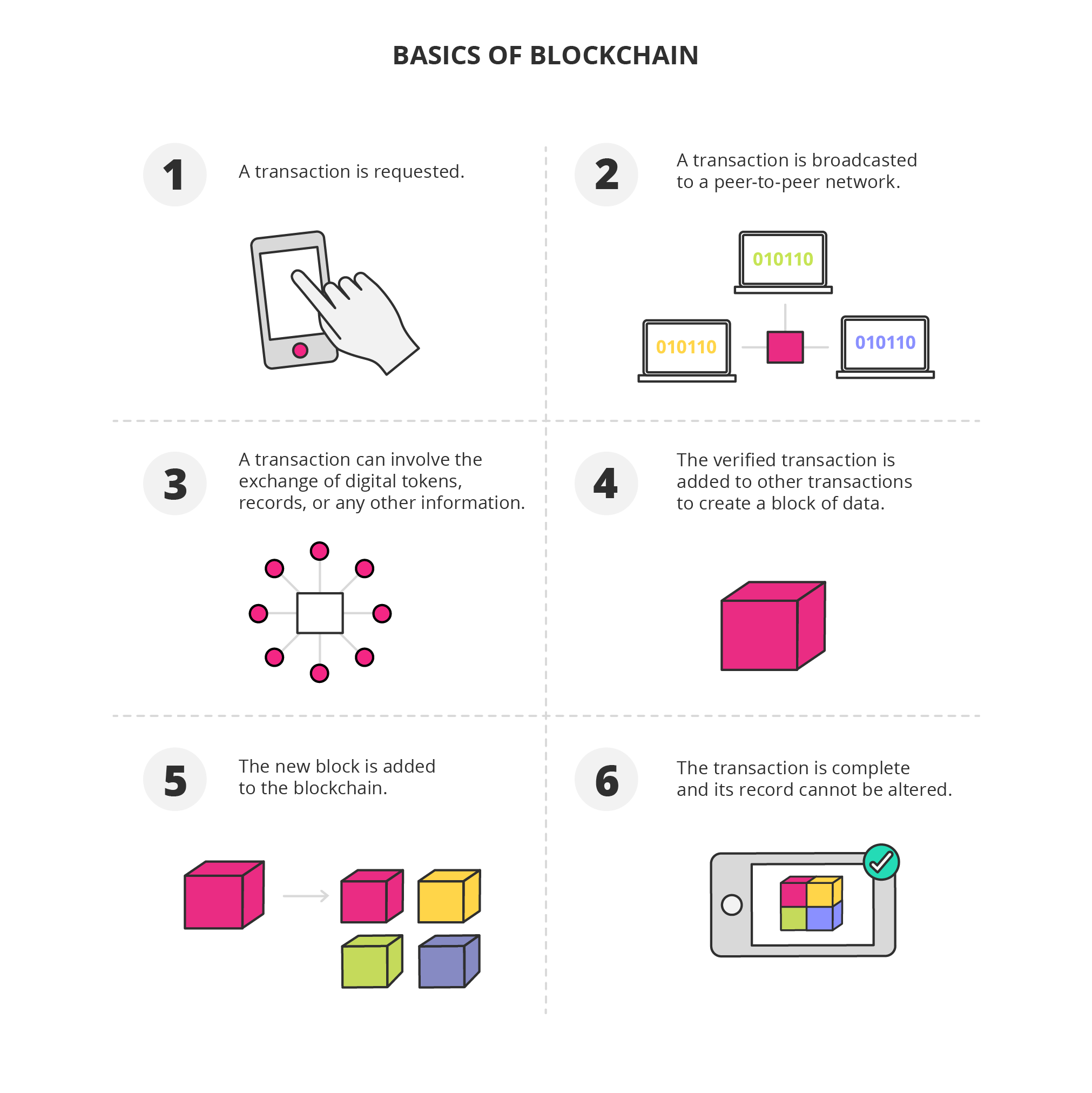

When a transaction is requested on the system, it’s broadcast to a peer-to-peer (P2P) network consisting of a number of interconnected computers, called nodes. Each of these nodes checks and validates the transaction for consistency across the network. Once validated, the transaction is grouped with other transactions to create a block of data for the ledger. These blocks are then grouped, logged, and linked in a chain with other blocks – a blockchain. Once logged, this chain is permanent and can’t be altered.5

Because the ledger is fully distributed across the network, it’s virtually incorruptible. To make a change in the ledger, you would have to log the change on every node across the entire network simultaneously. Otherwise, the network recognises one record doesn’t match the rest and it flags the transaction as corrupt. Every node on the network can access and make changes to the system simultaneously. Explained simply: hacking the blockchain is like trying to sneak through a single gate that’s being guarded by hundreds of watchdogs.6

Author and venture advisor, WIlliam Mougayar explains blockchain technology using an analogy with Microsoft Word and Google Docs. Our current system of banking works like Microsoft Word – when two parties try to edit the same document, the system locks one party out while the other is making changes. Two parties can’t view the same document at the same time. Banks do this all the time, temporarily locking the system while making transfers and adjusting balances.7

Blockchain, however, is like Google Docs. All parties can view and edit the same document simultaneously. The information is available to them at all times.

As Warburg explains, “The very thing that keeps the blockchain secure and verified is our mutual distrust. So rather than all of our uncertainties slowing us down and requiring institutions like banks, our governments, our corporations, we can actually harness all of that collective uncertainty and use it to collaborate and exchange more and faster and more open.”8

5 common misconceptions about blockchain:

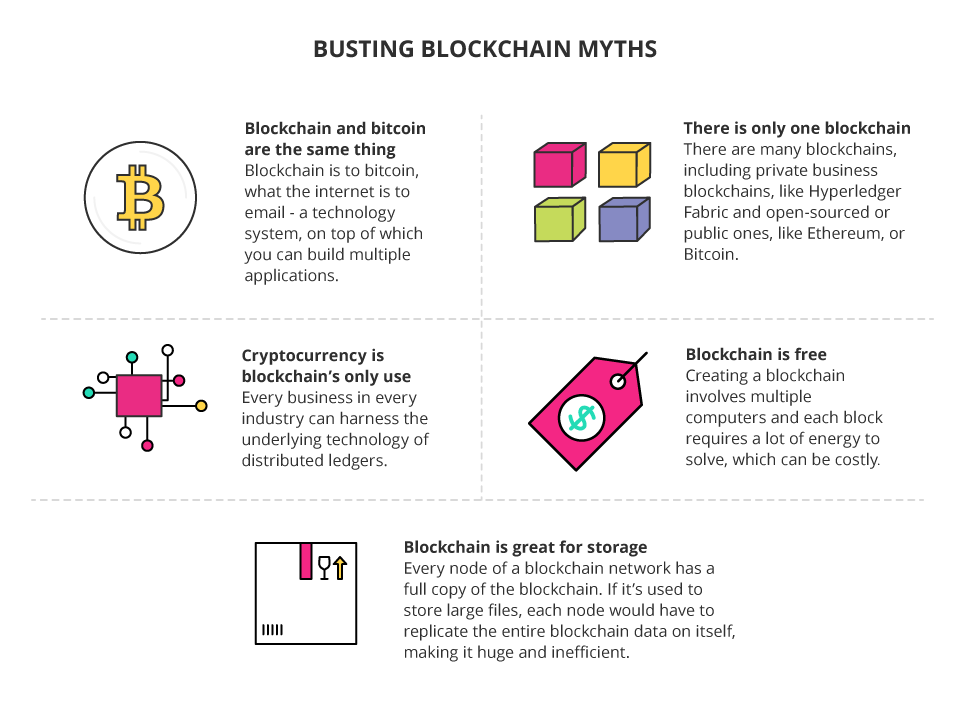

Myth 1. Blockchain and bitcoin are the same thing

Because bitcoin is more well-known than blockchain, people tend to think the two concepts are one and the same. In reality, bitcoin is merely an application of blockchain technology – one of many.9

Blockchain enables peer-to-peer transactions to be recorded on a distributed ledger throughout a network. Bitcoin is simply a cryptocurrency that uses blockchain to simplify online transactions and can be exchanged directly between two people without passing through a third party like a bank.

Myth 2. Cryptocurrency is blockchain’s only use

Beyond the potential of cryptocurrency, the technology behind distributed ledgers can benefit businesses in a number of different ways. One example of this is in the healthcare sector, where it can be applied to the entire value chain by using a secure public ledger to remove outdated and inefficient workflows.

The real estate market is also being affected by blockchain. Using smart contracts that allow buyers, sellers, and lenders to cut out the middleman could mean a quicker, more cost-effective alternative to the traditional process.10

Myth 3. There is only one blockchain

There are, in fact, many different types of blockchains, including private business blockchains, like Hyperledger Fabric, open-sourced or public ones, like Ethereum or Bitcoin, as well as federated blockchains.

In a public blockchain anyone in the world can participate and send transactions through the network. Transactions are transparent, but anonymous.11

Federated blockchains, on the other hand, operate under the leadership of a group. They don’t allow just any person with access to the Internet to participate in the process of verifying transactions. Federated Blockchains are faster and provide more transaction privacy.

Private blockchains use blockchain technology to set up groups and participants who can verify transactions internally. These are especially useful when it comes to scalability and state compliance of data privacy rules and other regulatory issues.12

Myth 4. Blockchain is good for data storage

Blockchain is actually not very effective for storing large amounts of data. The distributed nature of the blockchain means that every node of the blockchain network has a full copy of the entire blockchain. If it’s used to store large files such as video, each node would have to replicate all the blockchain data on itself, making the blockchain huge and extremely inefficient.

In reality, the blockchain is better used for recording transactional data as opposed to large files. Instead, large data files are usually stored outside of the blockchain and only the hashed address of the data file is stored on the blockchain itself.13

Myth 5. Blockchain is free

Creating a blockchain is an intensive process involving multiple computers solving complex mathematical algorithms. Each block requires a lot of energy to solve, which can be costly.14

According to Blockchain Luxembourg, the bitcoin cost per transaction has been between $75 and $160 since the beginning of 2018, in large part due to electricity costs.15

In addition to power, blockchains use a lot of storage – and storage requirements and costs will only continue to grow as each individual node must maintain a ledger of all transactions back to the start of each blockchain.16

“Many of the applications that have been proposed for blockchains – energy markets, music streaming services, IoT, and so on – will require storage of vast quantities of transactional information,” explains Jamila Omaar from the Interplanetary Database (IPDB) Foundation. “This is exactly the kind of data that should be stored within the blockchain database.”17

Applications of blockchain:

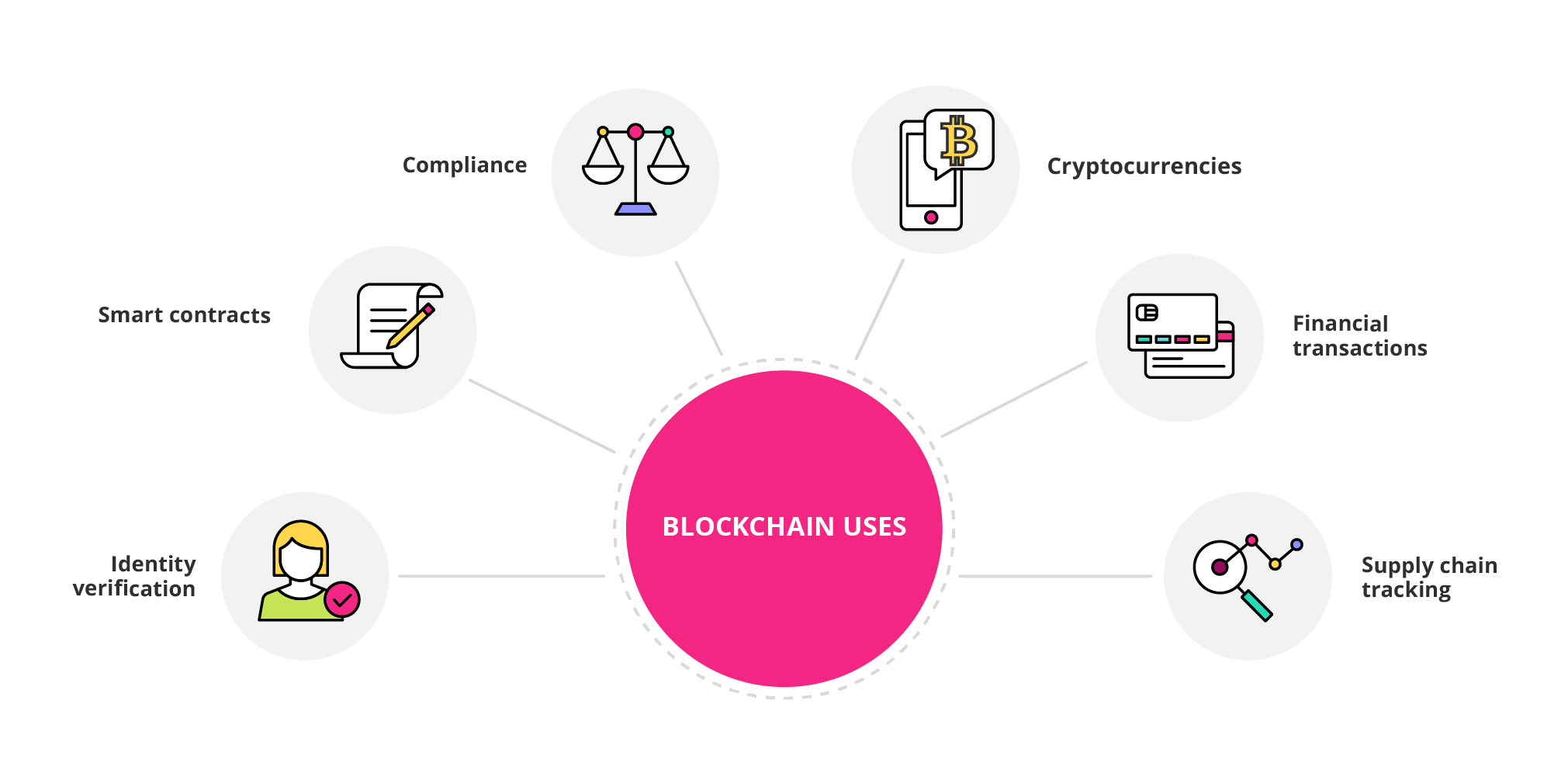

Smart contracts

Smart contracts are self-executing documents with the terms of an agreement between parties being directly written into lines of code. This results in automated transactions that are based on predetermined conditions. The code exists across a decentralised blockchain network and ensures the transactions are traceable, transparent, and irreversible. This removes the need for a central authority or external mediator.18 By side-stepping these middlemen, smart contracts could allow people to save on costs across a number of different industries.

Supply chain tracking

Supply chains have become difficult to navigate. It can take days to make a payment between different parties, contractual agreements generally require the use of expensive bankers or lawyers, and products are often hard to trace back to suppliers, making accountability a struggle.19

Blockchain technology could help give business owners better oversight of their vendors and suppliers by bringing more transparency to their supply chain. For example, BHP Billiton, the world’s largest mining firm, announced it will use blockchain to better track data throughout the mining process with its vendors. This will both increase efficiency internally, and help the company have more effective communication with its partners.20

Cryptocurrencies

Perhaps blockchain’s most well-known application is cryptocurrencies. Some of the most popular cryptocurrencies such as Bitcoin, Ethereum and Ripple have gained major interest in recent years among investors.21 However, their volatile nature has made investment in them potentially risky, leaving many people distrustful. Though it’s uncertain what the future holds for cryptocurrency, there’s still a large number of buyers, sellers, and service providers today who harness it as a simpler, less regulated form of online transactions.

Financial transactions

While blockchain is often mentioned in conjunction with cryptocurrency platforms like the ones mentioned above, the underlying technology goes far beyond this when talking about finance. The transfer of money has always been an expensive and slow process, especially for international payments. Because of this, blockchain’s most significant contribution to finance is perhaps not the advent of cryptocurrencies, but its ability to speed up and simplify this process while reducing the costs.22

By adopting a shared digital ledger, blockchain can allow banks to maintain a more accurate and up-to-date record of transactions, meaning faster access to funds for customers and faster processing for banks. According to a 2018 report by management consulting firm Accenture, this could allow the global banking industry to save as much as $20 billion by 2022.23

Identity verification

There’s a definite need for more effective identity verification online – having a secure identity is a crucial part of online interactions after all.24

Blockchain can be used to create a platform that helps reduce the risk of fraud and identity theft. It allows users to create encrypted digital identities that will replace their multiple usernames and passwords, while offering extensive security features that can save buyers and sellers valuable time and resources. Strong blockchains can also be employed in business to handle issues of authentication faced across a number of sectors.25

Compliance

Blockchain’s potential applications within legal and compliance frameworks have gained a lot of attention from companies operating in highly regulated industries in recent years.26 One of the most exciting features of blockchain from the compliance perspective is how immutable it is. As soon as data is added to the chain, it can’t be changed or deleted, meaning that blockchains can serve as a fully transparent and trusted system of record for regulators.27 Thanks to this, blockchain could remove many of the challenges businesses face in their efforts to keep up with today’s regulatory standards.28

Industry implications of blockchain:

By allowing digital information to be distributed but not copied, blockchain technology has created the backbone of a new type of internet.29 The system was originally devised for the exchange of cryptocurrencies like Bitcoin, but there are a plethora of other potential uses for the technology. These include:

Payment across borders

When employing remote workers or doing business in a global marketplace, business owners no longer need concern themselves with losing money on cross-national transactions.30 With no intermediaries slowing down the transfer of funds between banks and charging extortionate transaction fees in the process, business owners can leverage blockchain technology to transfer funds securely and directly to any vendor worldwide, instantly and at a lower rate.31

Cybersecurity

While the blockchain itself is public, the data is encrypted securely to prevent it being changed without authorisation. This could enhance cyber-defense by hindering fraudulent activities. Thanks to their distributed nature, blockchains have no central point of failure and are therefore more secure than many current database-driven transactional structures.32

Networking and the Internet of Things

When implemented as a central ledger for a large network of devices, blockchain technology allows the Internet of Things to operate more efficiently. Devices on the same network can communicate with one another directly instead of routing their updates through a central location.33

Insurance

Blockchain can be used to manage trust and verify data for insurance contracts. When personal insurance information is stored on the blockchain and claims are processed through the network, it reduces the possibility of fraud.34

Charity

Using blockchain technology to manage charitable donations ensures funds make it into the right hands, by removing the middleman and making transactions public.35

Voting

Elections can be made fair, democratic, and insusceptible to rigging by using blockchain to track voter registration and identity verification. Blockchain also provides an irrefutable record of all counted votes, making it impossible to fake or tamper with results.36

Healthcare

Using blockchain technology allows medical professionals to share medical records and patient information seamlessly. This ease of access can improve the speed and accuracy of diagnosis, ensuring the best possible patient care.37

Online Music

Blockchain-based solutions in the online music industry can help artists to get paid directly by their fans, removing the percentage-grabbing record company from the equation.38

Real Estate

In an industry where public documents and contracts are regularly shared between parties, blockchain technology can ensure transparency and reduce fraud. Blockchain applications like Ethereum allow for the development of smart contracts, or computer code which facilitates the exchange of value, monetary or otherwise.39

If your business relies upon trade, data, or technology to thrive, you can also leverage blockchain to prepare for future success – ensuring you not only adapt to this revolutionary change, but use it to your competitive advantage.

- 1 Warburg, B. (Jun, 2016). ‘How the blockchain will radically transform the economy’. Retrieved from TED.

- 2 Kharpal, A. (Jun, 2018). ‘Everything you need to know about blockchain’. Retrieved from CNBC.

- 3 (Dec, 2018). ‘Blockchain, explained’. Retrieved from Investopedia.

- 4 (Sep, 2018). ‘What is blockchain technology’, Retrieved from Blockgeeks.

- 5 Hassell, J. (Apr, 2016). ‘What is blockchain and how does it work’. Retrieved from CIO.

- 6 (Jun, 2018) How does blockchain work?. Retrieved from Investopedia.

- 7 Mougayar, W. (Nd). ‘Explaining the blockchain via a google docs analogy’. Retrieved from Startup Management.

- 8 Warburg, B. (Nd). ‘How the blockchain will radically transform the economy’. Retrieved from TED.

- 9 Marr, B. (Feb, 2018). ‘A very brief history of blockchain technology everyone should read’ Retrieved from Forbes.

- 10 (Oct, 2018). ‘10 misconceptions about blockchain technology’. Retrieved from Medium.

- 11 Buterin, V. (Aug, 2015). ‘On public and private blockchains’. Retrieved from Coindesk.

- 12 (Nd). ‘Blockchains and distributed ledger technologies’. Retrieved from Blockchain Hub.

- 13 Ram, P. (Aug, 2018). ‘5 common myths about blockchain and bitcoin’. Retrieved from Hackernoon.

- 14 (Aug, 2018). ‘12 myths about blockchain technology’. Retrieved from Datafloq.

- 15 (Jan, 2019). ‘Cost per blockchain transaction’. Retrieved from Blockchain.

- 16 Bloomberg, J. (Feb, 2018). ‘Don’t let the blockchain cost savings hype fool you’. Retrieved from Forbes.

- 17 Omaar, J. (Jul, 2017). ‘Forever isn’t free: The cost of storage on a blockchain database’. Retrieved from Medium.

- 18 Frankenfield, J. (Apr, 2017). ‘Definition of smart contracts’. Retrieved from Investopedia.

- 19 (Jan, 2019). ‘Blockchain technology is set to transform the supply chain’. Retrieved from Logistics Bureau.

- 20 Marr, B. (Mar, 2018). ‘How blockchain will transform the supply chain and logistics industry’. Retrieved from Forbes.

- 21 Hall, J. (May, 2018). ‘What is cryptocurrency? A simple guide to understanding cryptocurrency and crypto news’. Retrieved from Forbes.

- 22 (Nd). ‘5 blockchain technology use cases in financial services’. Retrieved from Deloitte.

- 23 (2018). ‘Building the future-ready bank: Technology vision for 2018’. Retrieved from Accenture.

- 24 (Sep, 2018). ‘What is blockchain technology’, Retrieved from Blockgeeks.

- 25 Pinto, R. (Jul, 2018). ‘How blockchain can solve identity management problems’. Retrieved from Forbes.

- 26 (Oct, 2018). ‘How blockchain will impact legal and compliance’. Retrieved from Medium.

- 27 (Nd). ‘How blockchain technology could change finance’.Retrieved from Coindesk.

- 28 (Oct, 2018). ‘How blockchain will impact legal and compliance’. Retrieved from Medium.

- 29 (Sep, 2018). ‘What is blockchain technology’, Retrieved from Blockgeeks.

- 30 (Nd). ‘How blockchain technology could change finance’.Retrieved from Coindesk.

- 31 (Nd). ‘5 blockchain technology use cases in financial services’. Retrieved from Deloitte.

- 32 Ravindra, S. (Jan, 2018). ‘The role of blockchain in cybersecurity’. Retrieved from Infosecurity Magazine.

- 33 (Jun, 2017). ‘19 industries the blockchain will disrupt’. Retrieved from Future Thinkers.

- 34 (Jan, 2019). How blockchain is disrupting insurance’. Retrieved from CB Insights.

- 35 (Jun, 2017). ‘19 industries the blockchain will disrupt’. Retrieved from Future Thinkers.

- 36 Liebkind, J. (Jun, 2018). ‘How blockchain technology can prevent voter fraud’. Retrieved from Investopedia.

- 37 Khurana, S. (Apr, 2018). How blockchain technology can transform the healthcare sector. Retrieved from Medium.

- 38 (Jun, 2017). ‘19 industries the blockchain will disrupt’. Retrieved from Future Thinkers.

- 39 (Sep, 2018). ‘What is Ethereum?’. Retrieved from Blockgeeks.